Today, let’s take a look back at how everything in 2007 was sunny until it wasn’t. And we will compare it with today’s data.

The current market situation, through the rhetoric and actions of the Fed—general narrative, interest rates, inflation, unemployment, etc.—is very similar to the state that preceded past crises.

Yes, history is not a guarantee that the future will be the same, but it is a guide that should not be ignored. It’s good to take at least the main lessons from it because listening to the general sentiment and talking heads on TV often doesn’t pay off. Those who now lament that the Fed is unnecessarily and excessively lowering rates will be the ones shouting the loudest in six months for the Fed to continue lowering them. Ignoring the past is like voting for Kamala Harris and expecting change and development. Sorry, white braindead dudes…

So, let’s get to the main message of today’s article: We will take a very detailed look at 2007 and how it all unfolded step by step. First, we’ll analyze 2007, and then compare it with 2024. After that, we’ll look at the financial “health” of the average US consumer and American companies.

Let’s go!!

CHAPTER 1: THE YEAR 2007

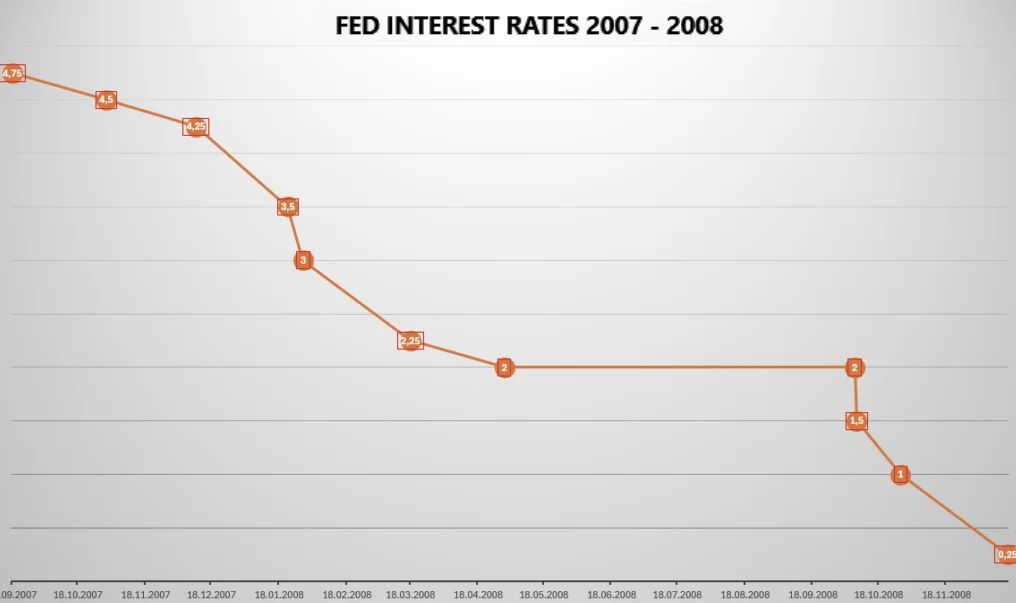

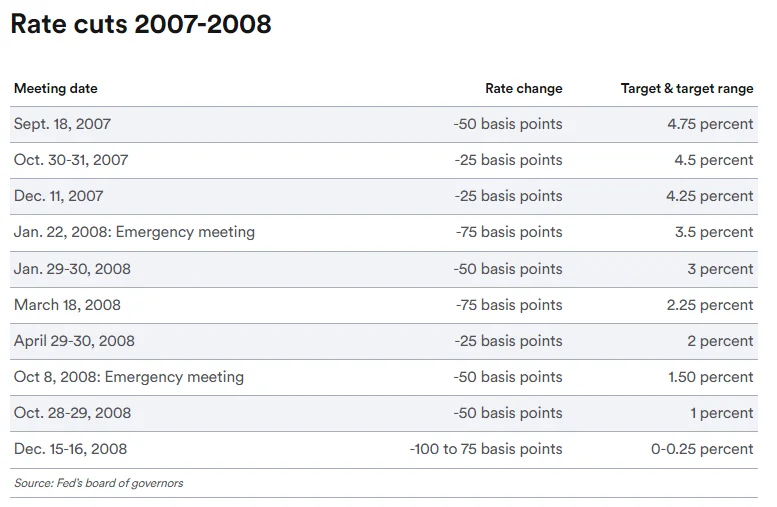

The first rate cut was at the September FOMC meeting on 18.9.2007 by 50bps to 4.75%. The market was shocked by this Fed decision because it expected a cut of only 25bps, and articles began appearing everywhere that the Fed was ahead of itself and would cause inflation and another endless stock market rise. The Fed succumbed to market pressure! Below is an excerpt from The NY Times article: